Home Equity Loan Calculator

Home Equity Loan Calculator

If you own your home, your equity is likely one of your biggest financial assets. Home equity is the difference between the total value of your property and the amount you owe on your mortgage. In essence, it's the dollar value of your home that's yours — not your mortgage holder's.

One of the benefits of having home equity is that you can borrow against it. For example, if you're considering significant expenses like home improvements or higher education, you can take a loan out against your home equity to get the money you need.

Taking out a home equity loan will create new debt, so you'll want to budget for your new monthly loan payments. That's where a home equity loan payment calculator comes in. Use the calculator to calculate your monthly loan payment and plan your finances.

What Is a Home Equity Loan and How Does It Work?

A home equity loan, or HEL, is a loan that uses the equity you have in your home as collateral.

For example, if you own a home worth $500,000 and have $400,000 left on your mortgage, you have $100,000 in home equity. You may qualify for a home equity loan of $75,000 or more.

Because your home is the collateral in home equity loans, you need to be careful. Your home could be at risk if you can't repay the loan. Other loan options, such as auto loans if you're buying a car, could be safer. Consider using an auto payment loan calculator to calculate your auto loan payment when you change different factors, like your down payment and repayment period.

Consider using personal loans or a credit card to cover smaller expenses instead of a home equity loan.

Fixed-Rate vs. Variable-Rate Loans

Home equity loans are available with either fixed or variable interest rates. If you have a fixed-rate home equity loan, your interest rate will stay the same throughout the loan. Your monthly payments will always be the same. With a variable-rate loan, your interest rate may go up or down based on market conditions, making your monthly payments less predictable.

Home Equity Loans vs. HELOCs

It's easy to confuse home equity loans with home equity lines of credit (HELOCs), but they're not the same. When you take out a home equity loan, you get the lump sum amount of the loan right away.

With HELOCs, you get approved for a total credit limit and have ongoing access to that money as needed. Your available credit replenishes as you repay the money you borrow against a HELOC.

Why Use a Home Equity Loan Payment Calculator?

Say you're considering a $50,000 home equity loan and want to know how much your monthly loan payments will be. Instead of guessing or roughly estimating, use a home equity loan payment calculator.

The calculator will calculate your monthly payment to help you figure out if the loan fits your budget. Just enter these key details about the loan:

- The loan amount (the total amount you're borrowing)

- The interest rate

- The repayment period

You can adjust these details until you find a combination that works for you. For example, if you decrease the loan balance, your home equity loan payments will be more affordable. A longer repayment period or lower interest rate will also reduce your monthly payments.

It's all about finding a balance between how much you want to borrow and how much you can afford to pay each month.

How To Use a Home Equity Loan Payment Calculator To Plan Your Finances

While shopping for home equity loans, you'll see offers with different interest rates, repayment schedules, and loan amounts. Use a home equity loan payment calculator to calculate your monthly payments with each loan offer. Seeing these direct comparisons will help you choose the best option.

You can also use the calculator to make budgeting easier. The calculator will show you how much you owe monthly, helping you stay within budget. For example, if you calculate payments on a loan for $30,000 and get a $500 monthly payment, you can start planning your finances to accommodate an extra $500 monthly expense.

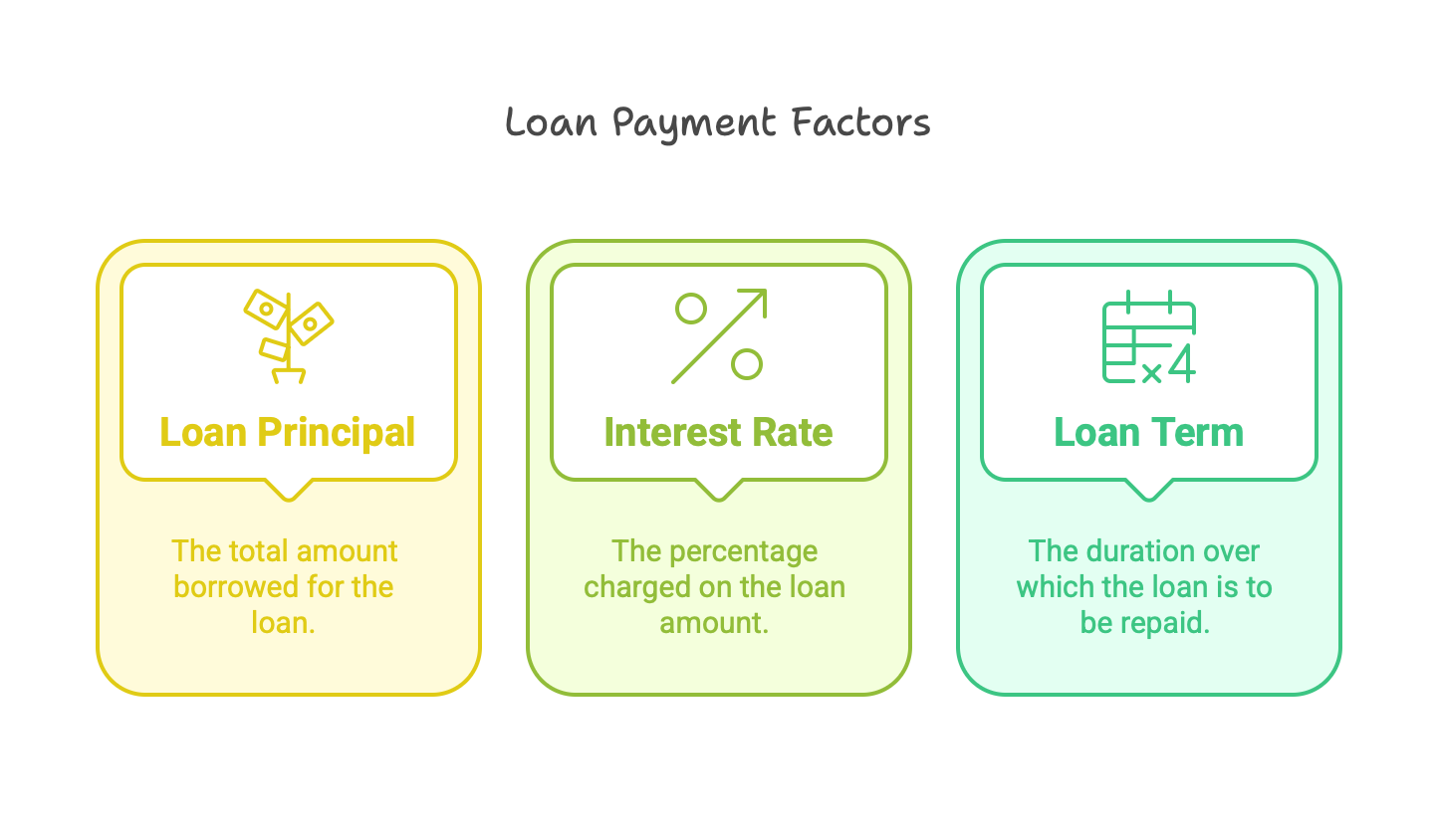

Factors That Influence Your Monthly Loan Payment

Three main factors influence your monthly loan payment: principal, interest rate, and loan term.

Loan Principal

Your loan principal is the total amount you borrow. Most lenders will only let you borrow up to 80% of the equity you have in your home, so that's your upper limit. Generally, the more you borrow, the higher your monthly payment will be.

Interest Rate

The interest rate is the percentage fee you pay on your loan principal to borrow money. A lower interest rate means borrowing is less expensive, so shop for lenders offering lower rates to save money.

Loan Term

Your loan term is how long you have to repay the loan. Longer loan terms mean your monthly payments are lower, but you'll pay more interest.

Consider closing costs and other fees associated with your home equity loan to get a complete picture.

Understanding Loan-to-Value (LTV) Ratio and Its Role in Loan Approval

Keep your loan-to-value ratio (LTV) in mind while evaluating loan options. Your LTV compares the amount you're borrowing against your home to the total value of your home. Calculate your LTV ratio using this formula:

LTV = Combined loan balance against the property / total property value

Make sure you add the remaining balance of your mortgage (if any) to the amount you want to borrow in a home equity loan when calculating your LTV.

For example, say you own a $500,000 home with a $250,000 outstanding balance in your mortgage. You want to borrow an additional $50,000 in a home equity loan. Your LTV would be ($250,000 +$50,000) / $500,000 = .60, or 60%.

Lenders typically view a higher LTV as riskier, so they may charge higher interest rates if you borrow against a greater percentage of your home value.

Choosing the Right Home Equity Loan for Your Needs

Each home equity loan is unique. With different loan amounts, interest rates, and repayment schedules available, it's worth shopping around and considering all your options.

Luckily, MoneyAtlas is here to help. Explore comprehensive loan comparisons to find the perfect one for your needs.